New Tax Year Tips from Church House Investment Management

Caroline Blatter 06 May 2021 Banking & Financial Services

With the start of the new UK tax year, how can you as Captains and crew keep more of your income for the future by making the most of allowances and tax reliefs? How can you make that money work for you rather than leaving it as cash in the bank to be eaten away by inflation?

We talk to Emma Parkes from Church House Investment Management for some professional insight:

Whilst you are working in yachting, hopefully qualifying for your Seafarers Earnings Deduction (SED) and therefore not paying tax on your earnings, it is really important to consider how those savings or investments will be taxed if you decide to return to the UK. It is naive to ignore this now, as you may be left with inaccessible investments or indeed unnecessary tax bills down the line. Take the opportunity of this new tax year to review your situation with your accountant or tax adviser.

Whilst working at sea and qualifying for your SED, you should still qualify for certain UK tax benefits. These should not be ignored:

1. ISAs (Independent Saving Accounts)

Build up a savings pot for a deposit on your first house, or longer term projects by maximising the allowance for tax-free investing, thereby boosting the return on your money.

There are 4 types of ISAs available:

Cash ISAs - low risk, however, due to historically low interest rates, the real value of your investment may well decline over time as a result of inflation. Allowance £20,000.

Stocks and shares ISAs - These are stocks and shares investment portfolios which utilise the ISA wrapper to make them tax efficient, as I have outlined above. Allowance £20,000.

Lifetime ISAs - You can open a LISA if you are over 18 and under 40. The Government will add a 25% bonus to your savings up to a maximum of £1,000 a year. The LISA limit is £4,000 per year and this counts towards your total ISA allowance of £20,000. You may not contribute to the LISA after 50 but cannot access it until you are 60, unless you use it to buy your first home. It is important for crew to note that you cannot use a LISA if your first property is a buy to let, or valued over £450,000, which may be restrictive.

Innovative finance ISAs - Only available to a restricted cohort of investors who meet certain criteria. High risk with limited protections, NOT covered by the Financial Services Compensation Scheme (FSCS). Allowance £20,000.

At Church House, we offer stocks and shares ISAs for clients wanting the opportunity to grow their investments and outperform cash. The portfolio can be accessed when required (i.e. not tied in to the LISA restrictions) and is fully protected by the FSCS. A range of risk scales is offered to meet the needs of cautious first time investors through to bullish long term investors seeking more aggressive capital growth.

2. Pensions

Don’t be the one to miss out on free money. Yes – you heard me, free money. If you do not want to be left working for ever, you ought to be planning your pension now!

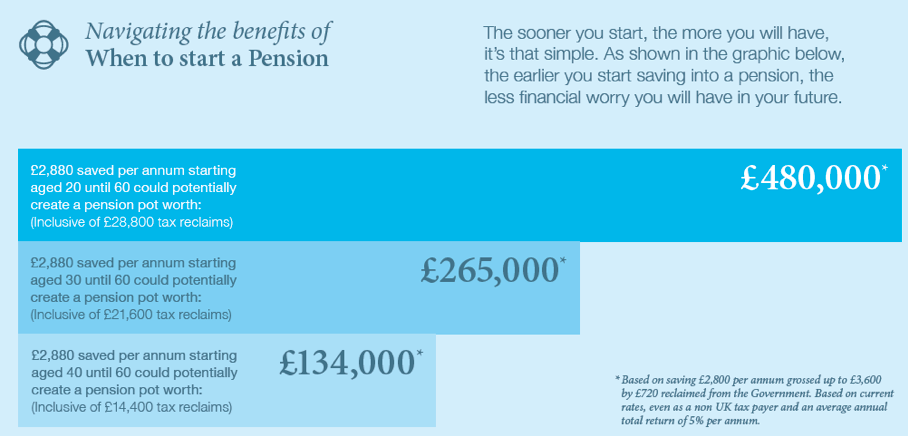

Whilst working at sea, you are still eligible to save the basic amount of £2,880 into a personal pension each year. The pension administrator will then arrange a tax reclaim from HMRC of £720 so that the gross contribution into your pension becomes £3,600. That’s right, £720 of free money. It might not seem much now, but look how this can grow:

As yachties, pensions are not provided as standard, so it is important that you take it upon yourself to investigate what is available to you and get saving early. It is of particular importance since you might well not be paying National Insurance and therefore may not qualify for a State pension. If you delay saving into a pension, you’ll need to contribute more to achieve a comfortable retirement. The sooner you contribute, the longer your money has to grow. The compounding effect of investment returns can make a massive difference over the long term as you can see. It is recommended that you consider consulting with an independent pension adviser.

3. Saving beyond ISAs and Pensions.

If you find you have savings over and above the ISA (£20k) and SIPP (£2,880) each year, you might consider opening a standard stocks and shares portfolio. Crew often forget that they do still qualify for the UK reliefs on savings and investments as follows:

Personal Allowance - you can earn £12,570 of UK income which includes investment income before you need to start paying income tax. You would need in excess of £400,000 invested at a yield of 3% to generate an income yield from dividends that would generate more than your personal allowance.

Dividend Allowance - In addition to the above, you also qualify to earn £2,000 per year from dividends before you are subject to tax. You only start paying tax on dividends once your personal allowance and dividend allowance have been used up.

Capital Gains Allowance - The capital gains allowance of £12,300 refers to the amount of profit you can earn from selling valuable items (including shares) before having to pay tax on it. So if you wanted to take money out of a portfolio for example, and you had used up your personal allowance and dividend allowance both of which apply to income, you might next consider selling down some capital to make the most of this allowance too.

The point to make here is that you can manage an onshore portfolio quite successfully using the available allowances offered by HMRC without having to employ complicated and often expensive offshore schemes. If you used up the 3 allowances above and had no other UK income, you could withdraw £26,870 per year from a UK portfolio tax free. Of course in specific circumstances, or with large portfolios, other planning options might be suitable, but do make sure that you explore the straightforward route first.

Keeping your investments transparent – and by that I mean not only having sight of your underlying investments but also being transparent with HMRC - will only make your life easier if you return to the UK. You should also ensure that your investments are liquid – i.e. you can access them when you need, and that they have adequate regulation and protections in place in case something were to go wrong. By investing in the UK with a regulated firm, you are minimising these risks.

So in summary:

- Aim to fill your ISA as far as you can - £20,000 per year. Consider a stocks and shares ISA so that your investments have opportunity for growth beyond inflation.

- Consider starting a pension and adding £2,880 a year and receiving £720 back from HMRC.

- For savings over and above this amount, a regular stocks and shares portfolio should be considered before expensive and complicated offshore schemes, which may commit you to excessive regular contributions, limited access and which may be complex and expensive to unwind should you return to the UK.

Don’t put it off get in touch to learn more!

CONTACT:

Emma Parkes

Tel: +44 (0)20 7123 4741

Email:e.parkes@church-house.co.uk

A wealth management service designed especially for yacht crew (ch-investments.co.uk)